In their 2013 Policy Reports, the West Virginia Chamber of Commerce advocates for the creation of a new tax loophole for businesses to avoid paying the state corporate net income and business franchise taxes. The Chamber wants the state to repeal the “sales throw out rule” and ensure that it is not replaced by a “sales throw back rule.”

Sales throw out and throw back rules prevent the creation of tax loophole known as “nowhere income.” When a business produces or sells goods in more than one state, it pays taxes to each state on a portion of its profit. The taxable share due to each state is determined by apportionment formulas in each state’s tax code, which assign some of the profit to the states where the goods are produced, and some to the states where the goods are sold.

However, federal law establishes a threshold level of presence or “nexus” a corporation must have in a state before it can be subjected to a corporate income tax on profit earned in that state. This can block a state from imposing an income tax on its share of a business’s profit if the business has only made sales in that state, and not produced anything. This creates “nowhere income” that is not subject to any income taxes, despite the goods being produced and sold in states with corporate income taxes.

State throw back and throw out rules address this loophole by allowing states to capture the nowhere income. The rules require businesses to either to subtract, or throw out, nowhere sales from total sales; or add, or throw back, nowhere sales to in-state sales. Either method affects the apportionment formula, increasing the income apportioned to the taxing state.

While the Chamber notes that only West Virginia and Maine employ throw out rules, 25 other states use throw back rules, accomplishing the same thing.

Repealing the sales throw out rule without a replacement throw back rule would further reduce taxes on businesses in West Virginia, which raises the question, can we afford to give more tax relief to businesses in the state?

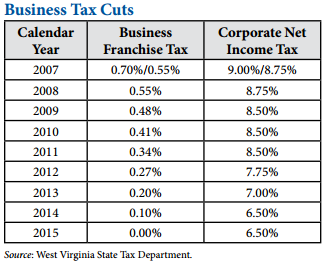

Remember, the states business franchise tax is in the process of being eliminated, the the corporate net income tax in falling from 9% to 6.5%.

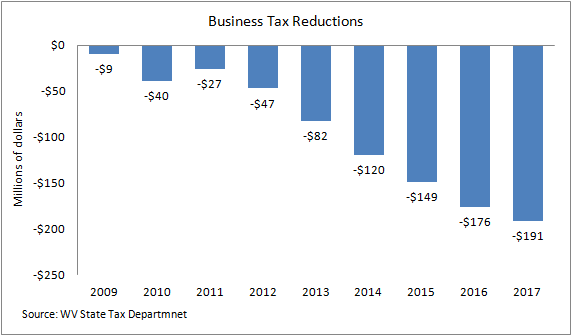

And these rate reductions will provide nearly $200 million per year in tax relief when fully enacted, and have already cost the state millions in forgone revenue.

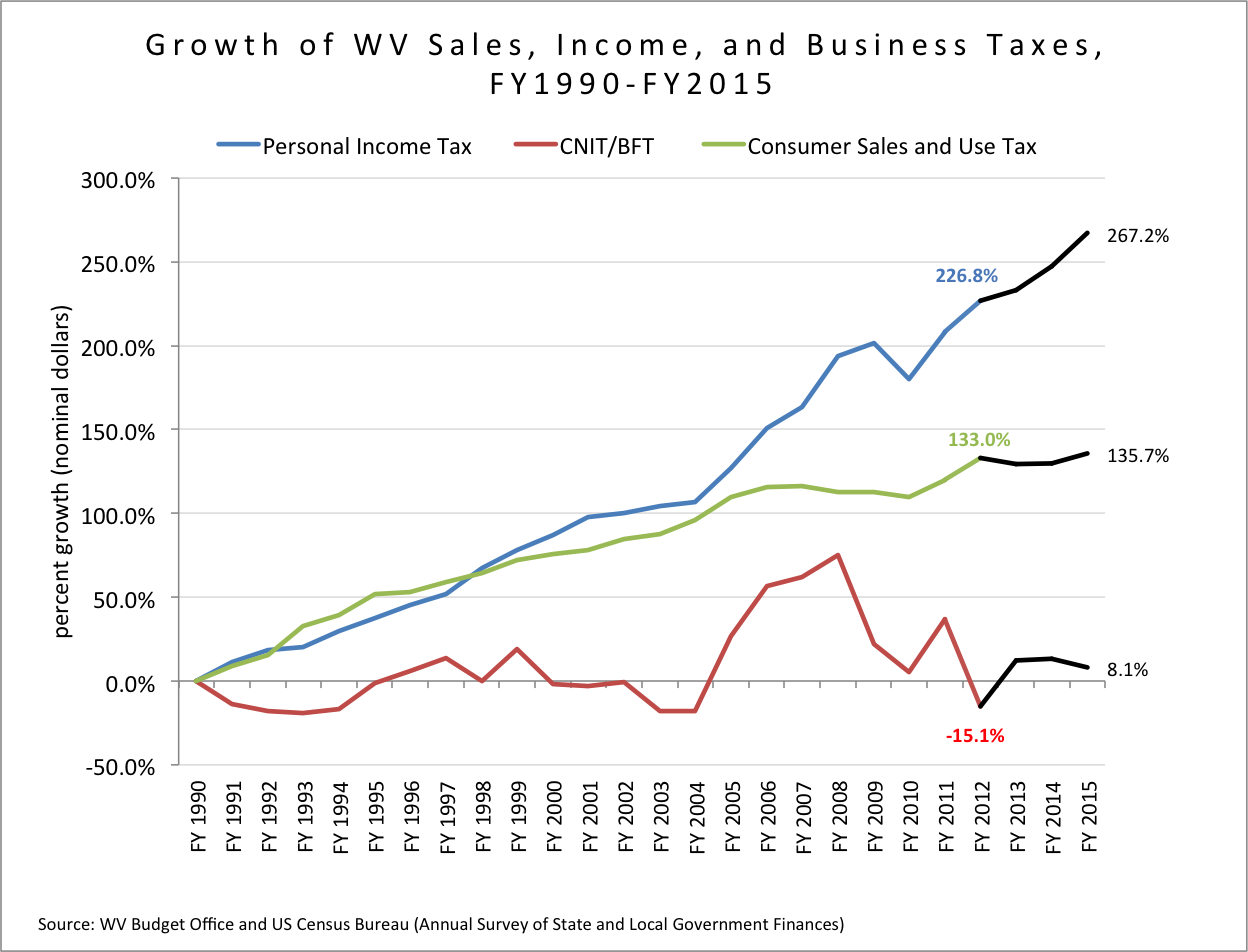

As a result, business tax collections have been falling sharply, making the state more reliant on personal income and sales tax revenue, with only rising severance tax revenue keeping the state from experiencing major budget problems.

Businesses in West Virginia have enjoyed hundreds of millions of dollars in tax relief over the past several years, and the state has nothing to show for it but

looming budget problems. The creation of more loopholes and giveaways will only create

more problems.