Today’s Daily Mail had an article about a proposed tax incentive designed to lure a potential “ethane cracker” to West Virginia. The proposal would reduced the assessment rate for property taxes from 60% to 5% for the cracker facility. This would dramatically lower the facility’s property tax burden, to the tune of about $500 million over the next 25 years.

So why does West Virginia need such a large tax incentive encourage a cracker facility to come here? According to Commerce Secretary Keith Burdette, it’s West Virginia’s dreaded business personal property tax. According to Mr. Burdette, “One tax that we aren’t automatically competitive in is personal property taxes because other states don’t have them — at least the states we are competing with don’t have them.”

As a refresher, most states have some sort of property tax, usually levied at the local level. While most states tax only real property (land and buildings), West Virginia also taxes business personal property (machinery, equipment, etc). This tax is a so-called job-killer, despite

little evidence of that being the case.

So since West Virginia taxes business personal property and other states don’t, we need to create expensive tax incentives because of that built in disadvantage, right? Well, it turns out that the disadvantage created by business personal property tax is easily cancelled out once you remember that West Virginia has incredibly low real property tax rates.

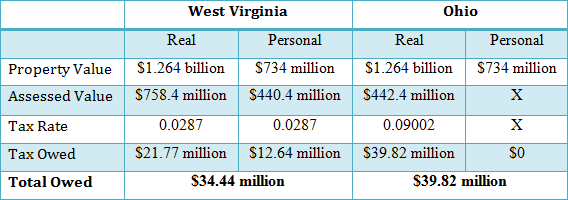

The cracker facility has an estimated value of about $2 billion. How much of that value is real property and how much is personal property is uncertain, but statewide property tax collections show that overall, about 63.3% of business property value is real, and about 36.7% is personal (see our

property tax primer). Using that ratio, our hypothetical cracker facility would have a real property value of $1.264 billion and a personal property value of $734 million.

So how uncompetitive is West Virginia? Let’s compare to one of our competitors for the cracker, Ohio. Ohio only taxes real property, applying an

average tax rate on business property of $90.02 per $1000 of assessed value, which is calculated at 35% of market value.

West Virginia taxes both real and personal property, applying an

average rate of $2.87 per $100 of assessed value, which is calculated at 60% of market value.

The differences in assessment values and levying rates can make direct comparisons tricky, and its easy to assume that since West Virginia taxes both real and personal, rather than just real, that its tax burden is higher. But that is not the case, as the table below shows.

As the Daily Mail article stated, the business community often complains about the business personal property tax, and if you only look at half of the chart you can see why. It shows the cracker facility paying $12 million in property taxes in West Virginia that it wouldn’t pay in Ohio. But if you look at the total property tax bill, West Virginia’s is lower. Why? The facility would pay an extra $18 million in real property taxes in Ohio.

How uncompetitive can the business personal property tax be when our real property taxes are almost half that of Ohio? The same is true for our other competitor for the cracker, Pennsylvania. Rates and assessments for PA were hard to come by, but on measure like property taxes per capita, as a percent of GDP, and as a percent of personal income, they were all much lower in West Virginia than in Pennsylvania, even though they don’t tax personal property there either.